24h在线客服

24h在线客服

备案号:辽ICP备19007957号-1

![]() 聆听您的声音:feedback@highmark.com.cn企业热线:400-111-0321

聆听您的声音:feedback@highmark.com.cn企业热线:400-111-0321

Copyright ©2015- 海马课堂网络科技(大连)有限公司办公地址:辽宁省大连市高新技术产业园区火炬路32A号创业大厦A座18层1801室

Since shadow banking is very popular in the modern world, it is worth to study the current development of shadow banking system throughout the world and evaluate the influences on financial system and stakeholders caused by the development of shadow banking. In the next sections, we will firstly define the term of shadow banking, review the current development of this new financial entities, and explain the attractions of shadow banking. Then the evaluation of the positive and negative effects of financial system and stakeholders will be conducted. In the end, the main points will be concluded and recommendations will be given for the further development of shadow banking.

There are many definitions of shadow banking and it is hard to decide which one is the best. In 2012, Financial Stability Board (FSB) described the shadow banking as “credit intermediation involving entities and activities (fully or partially) outside the regular banking system’’. And shadow banking can also be defined as non-banks which perform banking activities that are not regulated (Schmidt 2003). Both definitions have been applied in many papers and articles. However, these descriptions are more like a benchmark to justify the behavior of shadow banks rather than clear and precise definitions.

Claessenss & Lev Ratnovski (2014) defined shadow banking as “all financial activities, except traditional banking, which requires a private or public backstop to operate.’ This definition describes the characteristics of shadow banking activities today and the characteristics of future shadow banking activities.

Shadow banking can be best defined by exploring its development. There are two flaws about the definitions above. The first one is that there are some activities that are not supposed to be included into shadow banking, such as leasing and financing companies or corporate tax vehicles. Indeed shadow banking which originally encompassed leasing and financing including investment banking. These activities were provided by non-banks to support financing activities which were outside traditional banking. These activities are now embraced by banks as extension of the commercial banking activities.

Secondly, the location of shadow banking is described outside banks according to this definition. In reality, many shadow banking activities are conducted within banks. Many OFB (Off-Balance Sheet)) instruments are non-traditional banking activities. These activities consist of collateral operations of dealer banks, activities associated with repos, and so on. According to Cetorelli and Peristiani in 2012, this definition is less useful from operational point of view.

Another definition of shadow banking is considered from the functional point of view. This definition describes shadow banking as a collection of some particular intermediation services. In addition, each service was designed as a response for a demand. For instance, the demand for safe assets causes the occurrence of securitization, while collateral service is a response to the need of making full use of the scarce collateral which can support the secured transactions. The most important advantage is that this definition offers the insight views of the analysis of financial services. It reveals that the shadow banking is not only caused by the regulatory arbitrage, but also triggered by the general demand. Pozsar et al., in 2012 argued that based on this definition, if the government tends to regulate shadow banking effectively, the demands for these services and how these services are provided should be understood.

Given the existence of banks, there are still some attractions of shadow banking existence.

Firstly, the shadow banking as an intermediation is more efficient than traditional banks, and can offer healthy completion for existed banks. For example, the traditional banks are restricted in some sectors, thus there are some gaps in the financial markets. Then the shadow banking evolves and fulfills the gaps. As a result, the market becomes more efficient. Moreover, it is beneficial to the stability of banking system. The risks can be transferred from banking system to outside, and the investors are willing to hold these risks through market mechanisms. In fact, even though traditional banks and shadow banks have separate functions, they are interdependent. Shadow banking depends on the liquidity lines of traditional banks, while the traditional banks rely on shadow banks to fund through some special activities, which are not allowed in traditional banks (Lane, 2013).

The article of “Non-bank lending steps out of the shadows” in the Financial Times summed up the sentiments in the US of how shadow banks – business development companies – investment vehicle that support small companies with credit. (Financial Times, Dec 14, 2014)

The current financial environment is beneficial to further growth of shadow banking. There is an increasing of shadow banking activities in the United States, and Europe recently. Some activities are declining such as securitization, while some less risky activities display an increasing trending such as investment funds.

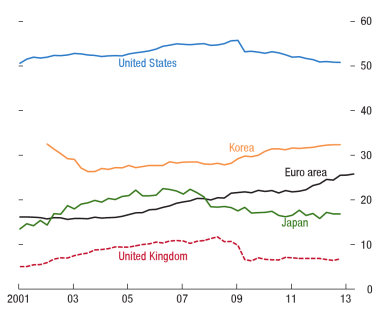

As banks retreat in the wake of the financial crisis, non-traditional banks are taking on a growing share of the business and supports growth. In the United States, the risks caused by the shadow banking activities kept rising, but at a pre-crisis level. Also, there is significant cross-border effects of shadow banking in developed countries by research evidence. By comparison, in emerging markets, the growth rate of shadow banking in China is particularly high. In Figure 1, we can see that percent of bank and shadow bank lending from 2001 to 2013 around the world (IMF, 2014). In the emerging markets, the increasing rate of shadow banking is higher than that of traditional banking. The reason of this growth in developing market is associated with rise in pension, sovereign wealth, and insurance funds (Lane, 2013).

Figure 1 Lending by shadow banks

(Source: national central banks and IMF staff estimates, 2014)

The definition of financial system is not very clear, like the definition of shadow banking. We consider it in narrow concept and broad concept two ways. Firstly, in narrow context, this term refers to the financial sector. It is a sector in the whole economy, which provides financial services to the other sectors. The important parts of this sector include central bank, commercial banks and other banks, financial institutions excluding banks, organized financial markets, and the regulation suthorities which supervise the financial activities. Secondly, we consider this term in broad context. This concept of financial system is defined as the interaction between the supply and the demand of capital. The banks act as the financial intermediations between the savers and the business. Instead of depositing money in banks, the savers can invest in the capital market in order to make profit bearing risks. At the same time, the business units also engage in the investment activities in the capital market. All the financial activities in the financial system are supervised by government and relevant institutions. The shadow banks we discuss in this paper outside the banks as another kind of financial intermediations between the savers and business units (Schmidt, 2003).

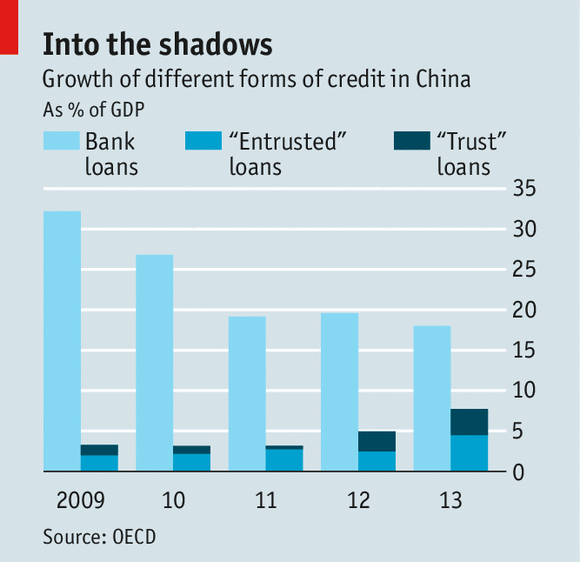

In China, shadow banks accounted for almost a third of the rise in lending last year, swelling by over 50% in the process in Figure 2. By offering returns, they raise money from businesses and individuals frustrated by the low cap the government imposes for interest rates on bank deposits. They lend to firms that are unable to borrow from banks with the curbs from the government.

Figure 2 Growth of different forms of credit in China

(Source: Financial Times (May 10th2014) “Shadow Banking in China”)

The main function of shadow banking is to transform the risk environment of simple process in the traditional banking into a more complicated financial activities environment. This can be attributed to the increasingly complex financial systems and the rising demand of various stakeholders. The original process of traditional banking is to deposit the money until maturity, and to lend money to make profits from the interest spread, which has a low return on equity. The financial activities of the shadow banks involve a more complicated, wholesale-funded, hold-to-sales, securitization-based, fee-driven lending. They have high return on equity (European Repo Council, 2012).

One positive impact of shadow banking on financial system is to stabilize the financial system as a whole. In terms of traditional banks, the borrowers and lenders can skip the intermediation and trade directly, which will results in losses of banks.

We call it the disintermediation of traditional banks. This in return will damage the efficiency of traditional banks and increase the costs of them. The securitization requires real credit risk transfer, which helps the issuer to diversify the loans, borrowers, and markets. The lenders can benefit from economies of scale of the structure of loans. In addition, the securitization is beneficial to the supervision of traditional banks by means of offering third party discipline and market pricing of assets (Pozsar et al., 2010).

With the existence of shadow banking, the financial system becomes more decentralized, which can help the system remain robust in the light of financial shocks. The reason is that the existence of shadow banks reduces the general sizes of most intermediations, and then prevents the business from concentration that makes the institutions into systemically important entities. The systemic risks of transmission can be alleviated by the diversification of functions.

The shadow banking can allocate the resources to the specific demands, which makes the funds allocation of financial system more efficient. The reason why shadow banks can do it is due to the increased specialization.

Thus, it is obvious that the existence of shadow banking enhances the efficiency of financial market and hence benefits both lenders and borrowers. It should be noticed for regulatory institutions that all the regulations are better to have particular target problems in case the damage of the functions of shadow banking would appear (Pozsar et al., 2010).

It is known that the traditional banking system is linked with the shadow banking system. Different from the positive side of shadow banking, some researchers argue that the interconnectedness of the shadow banking and traditional banking can increase contagion and systemic risks. Then, counter-party risks increased. As a result, the financial stability will be damaged by them. What is worse, the global financial crisis may occur (Jeffers & Baicu, 2013).

For instance, it is believed that one of the causes for the global financial crisis in 2008 is the rise of the shadow banking system. Fannie Mae and Freddie Mac, traditional housing mortgage institutions protected by the government, participated in financial instruments that belong to the shadow banking system, which have not been regulated in the traditional way. As a consequence, these two institutions bought large amount of mortgage loans, which provided liquidity to the secondary mortgages market and indirectly caused the sub-prime crisis. (Jeffers & Baicu, 2013).

Stakeholders of shadow banking are quite similar to the stakeholders of the financial system. The main groups of stakeholders in the shadow banking system include the governments, regulatory institution, traditional banks, large corporations and SMEs, financial institutions and ordinary investors.

The government agencies have responsibilities to make sure that the financial markets operate transparently and continuously. However, due the complexity of shadow banking system, the government and the regulatory institutions can hardly monitor the full operation of the system. The lack of transparency many lead to ineffective monetary policies and economic policies.

One positive impact of shadow banking on the stakeholders is that it provides more opportunities for market participants. For instance, the shadow banking can offer large corporations and SMEs with an alternative source of funding and liquidity (Baldoni & Chockler, 2011). Especially, when the corporations cannot satisfy the requirements of traditional banks, the shadow banks can finance the corporations with high liquidity. In term of the government agencies, it also provides alternative source of funds. For example, when there is a serious deficit in the government, the government agencies can finance themselves through shadow banking services instead of increasing taxes.

The existence of shadow banking offers liquidity for stakeholders and then reduce the relevant transactions cost associated with traditional banks. The high profitability and liquidity are the most important attractiveness for institutional stakeholders (Baldoni & Chockler, 2011).

However, based on above analysis, we can see that the shadow banking can accelerate and amplify the expansion of financial crisis. As a result, most of the financial institutional stakeholders will suffer from this financial crisis (European Repo Council, 2012).

Compared with traditional banking activities, the investments in the shadow banking sector is more attractive due to the high expected return. But the associated risks are also high accordingly. The existence of shadow banking can attract the financial institutions to take high-profit projects with high risks, which increases the default risks. In addition, since the financial institutional stakeholders can benefit from the shadow banking which is regulated less than traditional banks, the potential risks of regulatory agencies rise (European Repo Council, 2012). The existence of shadow banking increases the difficulty level of regulating the financial markets for regulatory agencies. In recent years, shadow banking in China remains a hot issue. The GDP growth of China is partially supported by the expansion of the scale of shadow banking in China Parker, 2012). It is reasonable to infer that if the Chinese governments take aggressive measures on regulating the shadow banking, the GDP growth of China may decline even further. For example, the lower GDP growth of 7% in China is attributive to the stricter regulation of shadow banking.

In conclusion, the shadow banking system is vital to the financial system and the global economy as a whole, with the retreat of traditional banks in the wake of the financial crisis (The Economist, May 10, 2014), thus it is worth studying. First of all, we discuss the various definitions of shadow banking. The functional approach gives us insight of this system, but it has difficulty in listing all activities.

Since the shadow banking can create a healthy competition environment and enhance the stability of financial system, the growth rate of shadow banking all over the world is very high. There are several advantages of shadow banking.

Firstly, it can stabilize the financial system. It provides alternative financing for those of need credit. Secondly, it can reduce the transaction cost and provide liquidity to stakeholders. However, there are many risks arising with the shadow banking, too.

In order to cope with the risks of shadow banking, regulators including the recommendations of Basel III bring up some recommendations rules and control over shadow banking activities. This could be healthy for the further development of shadow banking system.

First of all, there should be some more regulations and rules on the operation of shadow banking. These regulations are supposed to be designed with limitations. The limitation is that they cannot reduce the efficiency of shadow banking due to the gaps in the regulation area. For example, the interconnections between banks can be controlled to reduce potential risks.

For regulators, there are two issues to be concerned. Firstly, the maturity transformation is extremely serious when all savers withdraw their funds simultaneously. The second item is about the volume of credit extended. When the lent credit increases, the prices of assets rise, which indicates lower losses on credit extended. Thus, banks can lend more funds until the confidence crisis cause all the factors to move in the opposite directions (Claessens et al., 2012).

For the investors who participate in the market with shadow banks involve, it is suggested that they should pay more attention to the analysis of the investment projects, and consider the relevant risks associated with high expected returns. In particular, the idea of “too big to fail” must be watched out when investors assess the large financial institutions.

References

Baaldoni, R., and Chockler, G. (2011). ‘Collaborative Financial Infrastructure Protection: Tools, Abstractions, and Moddeleware.’ Springer.

Clasessens, S., and Ratnovsko, L. (2014). ‘What is shadow banking?’IMF Working Paper, 14/25.

Claessens, S., Pozsar, Z., Ratnovski, L., and Singh, M. (2012). ‘Shadow Banking: Economicsand Policy,’ IMF Staff Discussion Note 12/12 (Washington, D.C.).

Cetorelli, N., and Peristiani, S. (2012). ‘The Role of Banks in Asset Securitization’, Federal Reserve Bank of New York Economic Policy Review, 18, 2, 47-64.

European Repo Council.(2012). ‘Shadow banking and repo’, March, 2012.

Financial Stability Board.(2012). ‘Strengthening Oversight and Regulation of Shadow Banking’, Consultative Document.

International Monetary Fund.(2014). ‘Global Financial Stability Report-----Risk Taking Liquidity, and Shadow Banking’. Washington.

Jeffers, E., and Baicu, C. (2013).‘The Interconnections between the Shadow Banking System and the Regular Banking System. Evidence from the Euro Area’, City Political Economy Research Centre.

Lane, T. (2013).‘Shedding light on shadow banking’, CFA Society Toronto, 26 June 2013.

Schmidt, H. R. (2003). ‘What constitutes a financial system in general and the German financial system in particular?’ Working paper series: Finance and Accounting.

Financial Times (May 10th2014) “Shadow Banking in China”.

Pozsar, Z., Adrian, T., Ashcraft, A., and Boesky, H. (2012).‘Shadow Banking’, New York Fed Staff Report 458.

Parker, J. (2012). ‘Shadow Banking’ in China. [online] The Diplomat. Available at: http://thediplomat.com/2012/10/the-rise-of-shadow-banking-in-china/ [Accessed 17 Oct. 2012].

备案号:辽ICP备19007957号-1

![]() 聆听您的声音:feedback@highmark.com.cn企业热线:400-111-0321

聆听您的声音:feedback@highmark.com.cn企业热线:400-111-0321

Copyright ©2015- 海马课堂网络科技(大连)有限公司办公地址:辽宁省大连市高新技术产业园区火炬路32A号创业大厦A座18层1801室

hmkt088